What is 3D Secure?

3D Secure (3DS) is an authentication protocol designed to add an extra layer of security to online card transactions. Originally developed by Visa as “Verified by Visa” and later adopted by Mastercard as “Mastercard SecureCode,” 3D Secure has evolved into a global standard used by major card networks worldwide.

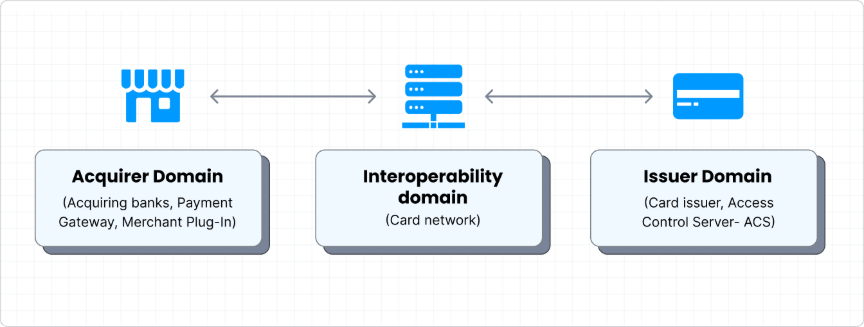

The “3D” refers to the three domains involved in the authentication process:

How Does a 3D Secure Payment Work?

3D Secure protocol adds an additional level of payment protection to an online transaction. The process requires cardholders to provide proof of identity before completing a purchase, ensuring that only authorized users can make transactions with their cards.

Business Benefits of 3D Secure

For payment gateway companies, implementing 3D Secure offers compelling business benefits that extend beyond basic fraud prevention. The technology has evolved into a strategic asset that significantly impacts merchant relationships, revenue protection, and competitive positioning.

Liability Shift Protection

3D Secure provides liability shift protection that transfers financial responsibility from merchants to card-issuing banks for authenticated transactions. When a transaction is successfully authenticated, merchants are no longer financially responsible for chargebacks, even if a customer later claims the transaction was unauthorized. The issuing bank, having verified the cardholder’s identity, assumes responsibility for the transaction’s legitimacy.

Merchants also benefit from reduced administrative burden and can keep revenue from legitimate transactions that might otherwise have been lost to chargebacks.

Regulatory Compliance

The European Union’s PSD2 requires Strong Customer Authentication (SCA) for most online payments, and 3D Secure 2.0 is the primary method for meeting these requirements. For payment gateway companies, offering 3DS2 compliance is essential for serving merchants in regulated markets. PSD2 requires two-factor authentication, and 3DS2 provides a framework that meets these requirements while maintaining a smooth user experience through frictionless authentication for low-risk transactions.

Fraud Reduction

3D Secure employs multi-factor authentication to verify cardholder identity, ensuring only authorized users can complete transactions. The technology incorporates sophisticated risk assessment that challenges only suspicious transactions while allowing low-risk transactions to proceed seamlessly. The system collects comprehensive data about transactions, devices, and cardholder behavioral patterns, enabling issuing banks to make informed decisions about whether additional authentication is required.

Improved Authorization Rates

3D Secure 2.0 improves transaction authorization rates by providing issuing banks with rich, comprehensive transaction data that enables more accurate risk evaluation. Traditional payment processing often results in legitimate transactions being declined due to insufficient information, but 3DS2 addresses this by collecting detailed information about each transaction, including device characteristics, transaction history, and behavioral patterns.

Enhanced Customer Trust

3D Secure provides visible security measures that significantly impact customer confidence. The technology offers a transparent, branded authentication process that demonstrates the merchant’s commitment to security. When customers see the familiar authentication page from their trusted bank, they gain confidence that their transaction is being processed securely.

Conclusion

3D Secure has become a vital tool for secure, compliant, and high-performing online payments. By reducing fraud, shifting liability, improving approval rates, and strengthening customer trust, it provides clear financial and competitive advantages. For payment gateways and merchants alike, adopting 3DS2 is now essential for protecting revenue and delivering a safer, smoother checkout experience.