Buying a home is a significant milestone, marking both a major financial investment and a cozy haven for you and your loved ones. While there’s so much joy in homeownership, it also comes with some important responsibilities, especially when it comes to keeping your home and belongings safe. That’s where homeowners insurance comes into play! In this guide, we’ll clarify the key factors affecting your home insurance costs, what is typically not covered, how to estimate premiums, common myths, and tips for lowering those costs. Let’s dive in and make sure your home is well-protected!

1. Factors affecting the premium

To accurately estimate the policy price, a bunch of factors are taken into consideration. These are some most important factors that you should think about when estimating your policy:

- Location: Your home’s geographical area plays a significant role. Insurance companies track the number of claims, type of claims, and the cost of claims in each postal code area. Higher premiums are common in flood and earthquake-prone locations and high-crime neighborhoods.

- Property value: The total value of your home and its contents directly affects your insurance cost. Higher-value homes typically require more coverage.

- Age and construction of your home: Characteristics such as the age of your home, construction materials, and safety features (like alarm systems) can influence premiums. Homes equipped with advanced safety measures may qualify for discounts.

- Claim history: Claims affect your home insurance premium. Being claims-free assists in reduced rates with discounts on your home insurance premium of 10% to 15%. Property claims stay on your record for 5 years, and most home insurance companies allow a claims-free discount once you are claims-free for 3 years or more.

- Credit score: Many insurers consider your credit score when calculating premiums. A higher score often results in lower insurance costs.

2. What is not covered by home insurance?

You may think your insurance is all-encompassing, but it is surprising to learn that certain risks and damages are excluded from the policies. Some of them are listed out below:

- Flood and earthquake damage: Most standard policies do not cover damages from floods or earthquakes. Separate policies may be needed for these risks.

- Wear and tear: General maintenance issues and normal wear and tear are not covered, including aging roofs and plumbing issues.

- High-value items: Standard policies often have limits on coverage for high-value items like jewelry or art, requiring additional riders for full protection.

- Government action: The cost of replacing your home or possessions if they are damaged or destroyed by a governmental entity is not covered.

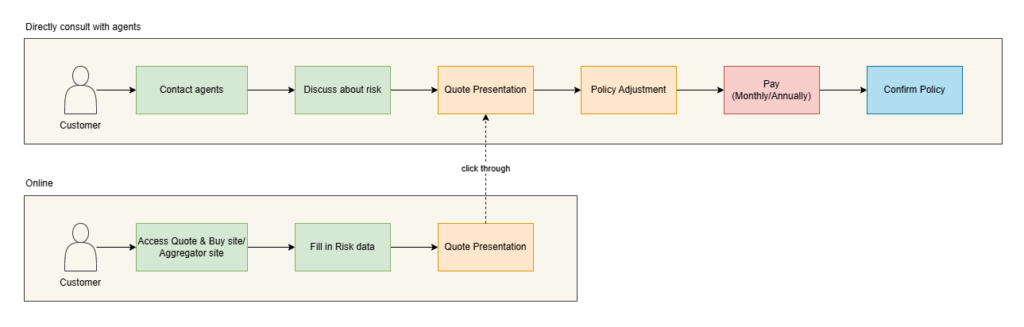

3. Where can you get a home insurance quote?

There are two main ways for you to estimate your quote: online and offline. Let’s see the user journey flow:

- Online: You can access directly to Quote & Buy site to calculate the price. Besides, aggregators are becoming popular in this digital ages. They not only calculate the premium but also compare prices between many providers, so that you can choose the best one. For example, Compare the Market is now become a famous aggregator in UK.

- Directly consult with agents: You can easily contact agents about your demand. The agents will help you to calculate the premium and give you some advice based on your preferences.

4. Some Common Myths About Home Insurance

Many homeowners hold misconceptions about home insurance that can lead to inadequate coverage. Understanding the truth behind these myths is crucial for effective protection.

- Home insurance covers everything: Many believe their policy covers all types of damage. In reality, policies often have exclusions.

- You don’t need insurance if your home is paid off: You may believe they don’t need insurance once their home is paid off, but this leaves them vulnerable to significant financial loss. Although you pay off your house, you should still protect their property against risks like fire, theft, or natural disasters.

- Renters don’t need insurance: Renters often think they don’t need insurance because the landlord has coverage. However, the landlord’s policy does not cover personal belongings.

- Filing claims will always raise your premiums: While this can occur, it’s not always the case. Some insurers offer loyalty discounts and may not raise premiums for small claims.

- Home insurance is a waste of money: Home insurance is a crucial investment that protects your property and finances from unforeseen events.

5. Tips for Lowering Premiums

Lowering your home insurance premium can save you money without sacrificing coverage. Here are some practical tips to help you lower your home insurance premiums:

- Enhance home security: Installing security systems, smoke detectors, and deadbolt locks can make your home safer and may qualify you for discounts.

- Increase your deductible: Opting for a higher deductible can lower your premium, though you’ll need to pay more out-of-pocket if you file a claim.

- Bundle insurance policies: Consider bundling your home insurance with auto or other types of insurance for multi-policy discounts.

- Maintain a good credit score: A higher credit score can lead to lower premiums, so focus on managing your credit responsibly.

- Review and update your policy regularly: Ensure your coverage reflects any changes in your home or belongings, and shop around for better rates every few years.

6. Conclusion

To effectively understand your home insurance premium, it’s essential to recognize the key factors that influence costs, identify what your policy doesn’t cover, and accurately estimate your premiums. Additionally, debunking common myths about home insurance can empower you to make better decisions. By implementing the cost-saving tips outlined in this guide, you can potentially lower your home insurance premiums while ensuring you have the right coverage for your unique needs. Always consult with insurance professionals to make informed choices about your home insurance policy.