Have you ever wondered what sets online bank transfer transactions apart from credit card transactions? Let’s dive into the payment industry and learn some interesting information.

First, let’s take a look at the sequence diagrams for these two payment scenarios:

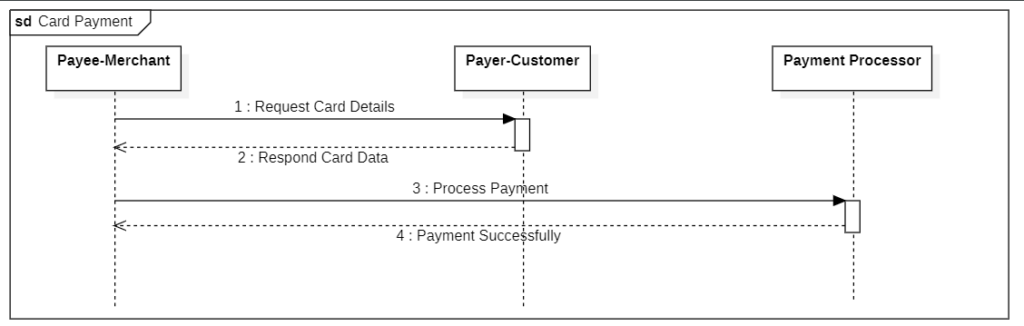

Card Payment Process

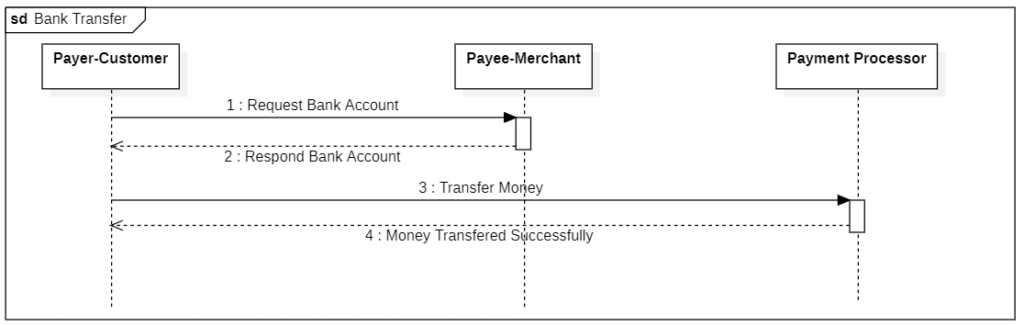

Bank Transfer Process

Can you guess the differentiator? Here’s a clue: Where is the trigger point? In bank transfers, the sender takes charge and initiates the funds’ transfer, whereas credit card processing involves the merchant capturing card details and forwarding them to the acquirer’s network to pull the funds. These distinct methods are often referred to as “push” and “pull” systems.

The Push System

Imagine the payer confidently initiating the payment transaction, providing authorization and instructions to their financial institution. With a simple instruction, funds flow from the payer’s account to the according payee. The pull system includes credit card payments, direct debits, and automated clearinghouse transfers. It thrives in scenarios involving recurring payments, subscriptions, and online purchases.

The Pull System

Now, imagine you’re the payee. You want to receive a payment, so you kick things off in the push system. You request the payment from the payer, who then gives the green light for the funds to be transferred. Mobile payment apps, person-to-person transfers, and digital wallets are all popular examples of push systems. They’re perfect for instant payments, peer-to-peer transactions, and mobile commerce.

So, which one is better?

Well, push payments tend to be less risky and more cost-effective. When you push a payment, you’re the one initiating it, and the transaction won’t even start if there aren’t enough funds in your account. Plus, once a push transaction goes through, the beneficiary can be pretty sure they’re getting their money – not reversable! Push payments are also more wallet-friendly, requiring less compliance and being cheaper to use.

On the other hand, pull payments can be a bit riskier. Merchants have to deal with credit risks, making them pricier. As a consumer, you have less control over your funds in pull payments. Particularly in situations where the payer might unintentionally initiate the transfer – such as lost cards or scams, and then the transaction is reversed (or chargeback). In order to tackle such challenges, there are some technology innovations in places to improve the authentication process for online credit card transactions, called 3D Secure which requires at least 2 out of 3 factors to verify cardholders including:

- Knowledge: Something only the payer knows (PIN, password or memorable information)

- Possession: Something only the payer possesses (card, mobile device or keyfob)

- Inherence: Something only the payer is (fingerprint, face recognition or voice)

In summary, while there are other types of payment methods available, such as contactless payments and mobile payments, understanding the two fundamental payment flows of pull and push payments is essential to understanding how payments work in the digital age.